YAOUNDE, Cameroon, March 24, 2025/APO Group/ –The African Development Bank Group (

www.AfDB.org) has given the green light to a loan of €330.48 million to Cameroon to redevelop and widen a key section of the Douala-Ndjamena economic corridor, a vital part of plans promoting strengthened regional integration.

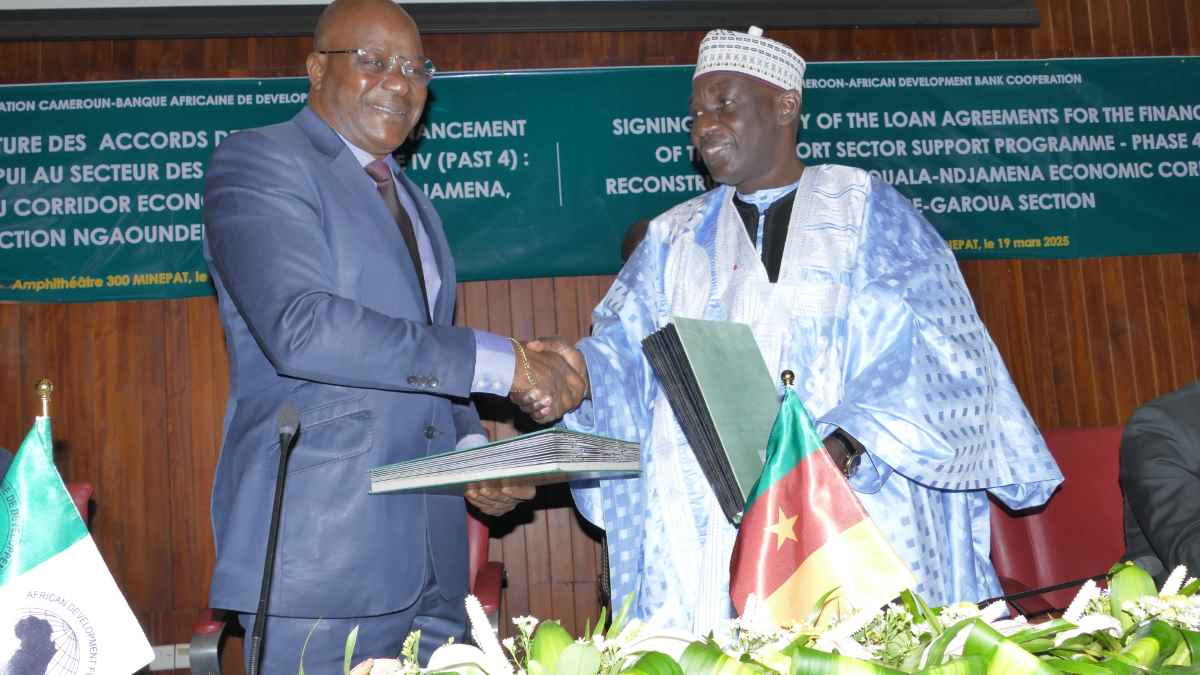

The financing agreement for the 246-km-long Ngaoundéré-Garoua section of the Douala-Ndjamena economic corridor, one of the most strategic corridors in Central Africa, comes under part of Phase 4 of the Transport Sector Support Programme (PAST4).

It was signed on 19 March 2025 in Yaoundé by Solomane Koné, the African Development Bank Group’s Acting Director General for Central Africa, and Alamine Ousmane Mey, Minister of Economy, Planning and Regional Development and Governor of the Bank for Cameroon.

“The redevelopment of the Ngaoundéré-Garoua road section is crucial to the competitiveness of our economy, due to improved connectivity and easier movement,” said Mey. “[…] It will also enable us to make better use of the agro-pastoral and commercial potential of the areas it crosses, to the great benefit of local communities.”

Koné added: “Phase 4 of the Transport Sector Support Programme, approved by the Board of Directors of the African Development Bank on 13 December 2024, was designed to amplify the impact of the Bank Group’s previous actions and to support its leadership and its dynamic cooperation with Cameroon within the transport sector.”

The ceremony was attended by Hilarion Etong, Senior Deputy Speaker of Cameroon’s National Assembly, and several members of the government, including Jean Ernest Ngallé Bibéhè, Minister of Transport, Emmanuel Nganou Djoumessi, Minister of Public Works, and Ibrahim Talba Malla, Minister Delegate to the Presidency in charge of Public Contracts, as well as local elected representatives and governors of regions such as Adamaoua and the North.

The Bank Group will provide 97 per cent of the total cost of Phase 4 of the Transport Sector Support Programme, which amounts to €340.7 million. The Government of Cameroon will contribute €9.14 million.

The aim of the programme is to modernise a strategic section of Cameroon’s road network, which is essential for transporting people and goods between the north and south of the country. To enhance traffic flow, three interchanges are also planned. The programme includes measures to improve transport and support local residents, specifically through the construction of socio-economic infrastructure such as markets, schools and health centres. Bringing this stretch of road up to international standards will have a highly positive impact on the competitiveness of the economy and the dynamics of integration in the sub-region.

“Cameroon’s geostrategic position places our country at the core of the integration challenges facing the CEMAC (https://apo-opa.co/41UocZF) (Economic and Monetary Community of Central Africa) region,” explained Mey. “An improved Ngaoundéré-Garoua section will undoubtedly boost cross-border trade by significantly increasing traffic on the Garoua-Maroua-Kousseri-Ndjamena road (in Chad) and the Garoua-Magada-Yagoua-Bongor-Ndjamena road.”

Phase 4 of the Transport Sector Support Programme is in keeping with Cameroon’s National Development Strategy for 2020-2030 (SND30) and the Bank Group’s priorities in Cameroon’s Country Strategy Paper for 2023-2028, which is aligned with the objective of diversifying Cameroon’s economy, in particular by facilitating access to markets for agricultural and industrial producers in the north of the country.

The African Development Bank Group and Cameroon are strategic partners, particularly in the infrastructure sector, with investments of $1.88 billion in transport infrastructure. The Bank Group’s commitment is reflected in major investments in the construction and upgrading of roads, bridges and strategic corridors, thereby facilitating the movement of people and the transport of goods on a national and regional scale. By adopting an integrated and inclusive approach in line with its Ten-Year Strategy 2024-2033, the Bank Group is stimulating the structural transformation of the economy and regional integration, with a view to sustainable growth and job creation for the benefit of inhabitants.

Business4 days ago

Business4 days ago

Business4 days ago

Business4 days ago

Business4 days ago

Business4 days ago

Business3 days ago

Business3 days ago

Business3 days ago

Business3 days ago

Business3 days ago

Business3 days ago

Business3 days ago

Business3 days ago