Business

Nigeria signs Intra-African Trade Fair 2027 host agreement; gears up for Africa’s biggest marketplace

Published

5 months agoon

Nigeria to host the fifth Intra-African Trade Fair 2027 (IATF2027) from 5 to 11 November 2027

The agreement signing ceremony was held in Lagos, the designated ‘host city’, in partnership with African Export-Import Bank (Afreximbank), the African Union Commission and the African Continental Free Trade Area (AfCFTA) Secretariat, reinforcing Nigeria’s central role in advancing Intra-African trade and economic integration across the continent.

Scheduled to take place from November 5 – 11, 2027, IATF2027 is targeting over US$50 billion in trade and investment deals, 100,000 visitors, 2,500 exhibitors, and participation from more than 100 countries. The Fair will be held under the theme “Global Africa, Smart Trade- From Market Access to Market Power” featuring diverse programme notably the trade exhibitions; AfCFTA-focused trade and investment forum; the Global Africa Day to strengthen ties with Africa’s diaspora; a B2B (Business-to-Business) & B2G (Business-to-Government) platform; Creative Africa Nexus (CANEX) to showcase Africa’s creative economy; the Sub Sovereign Governments Network for regional and local governments integration; special days for countries, public and private sector to showcase their trade and investment potential, tourism and cultural highlights; Africa Automotive Show; AU Youth Start-up pavilion for African youth start-ups; and the Africa Research & Innovation Hub (ARIH) for academia and researchers.

In just four editions since 2018, IATF has cumulatively generated over US$167 billion in trade and investment deals and welcomed more than 180,000 visitors from 132 countries. This strategic partnership creates a uniquely African framework that blends policy direction, financial backing, and trade facilitation. IATF benefits from continent-wide institutional alignment, setting it apart in both structure and purpose.

Delivering his opening remarks, H.E. Chief Olusegun Obasanjo, Chairperson of the IATF2027 Advisory Council and Former President of the Federal Republic of Nigeria, underscored the strategic importance of the Fair in shaping Africa’s economic sovereignty.

“The signing of this host agreement marks a momentous milestone for Nigeria and for the continent. Bringing IATF2027 to Lagos is historically significant, as this city hosted the Lagos Plan of Action adopted in 1980, which championed Africa’s industrialisation and economic self-sufficiency. We have to work hard to keep moving towards the Africa we want. I am confident that IATF2027 will surpass all previous editions in both scope and impact as we advance our shared goal for a unified African marketplace under the AfCFTA,” he remarked.

Commenting on Nigeria’s expanding footprint in intra-African commerce, H.E. Dr. Jumoke Oduwole, Federal Minister of Industry, Trade and Investment, highlighted Nigeria’s rising contribution to continental trade flows.

Together, we must align our markets, our industries and our talent to deliver the prosperous Africa we envision

“Today, as the international trading system faces profound challenges, we must remain resolute in our commitment to mutually beneficial, rules-based trade. As we prepare to host Africa’s largest marketplace in Lagos in 2027, we have an opportunity not only to reflect on our reality but to design the future of African trade integration and economic transformation. The work ahead of us under the AfCFTA is not only expansive but also existential for our survival and prosperity. IATF 2027 will therefore be a defining moment in accelerating and transforming intra-African trade and investment. Together, we must align our markets, our industries and our talent to deliver the prosperous Africa we envision,” she affirmed.

Appreciating Nigeria’s longstanding partnership and leadership in advancing intra-African trade, Dr. George Elombi, President and Chairman of the Board of Directors of Afreximbank, commended the Government’s commitment to the AfCFTA vision, noting that Nigeria’s scale, entrepreneurial depth, and industrial capacity make it a natural host for the 2027 edition.

“Nigeria’s vibrant entrepreneurial spirit gives us confidence that IATF2027 in Lagos will be a remarkable event that strengthens trade and investment across the continent. The trade fair is about building a strong pan-African single market and expanding intra-African trade beyond the levels we see today. Our collective duty is to use this platform to build value chains, create jobs and generate prosperity for our people. When Africans decide to work together, as they will at IATF 2027, the opportunities for transformation are limitless,” he highlighted.

Nigeria remains central to the success of AfCFTA, not only because of its market size but also due to its resource base and industrial potential. As a leading producer of oil and gas, solid minerals, including limestone, iron ore, gold, and lithium, and key agricultural commodities, Nigeria combines industrial capacity with a vibrant SME sector and a dynamic role in intra-African trade. This unique mix positions the country to drive value chains that power regional integration and strengthen the continent’s economic resilience.

Describing Nigeria as a major contributor to African Union growth and regional economic transformation, H.E. Francisca Tatchoup Belobe, AU Commissioner for Economic Development, Trade, Tourism, Industry and Minerals, highlighted the importance of aligning industrial policy, mineral development, and trade facilitation to unlock Africa’s full potential.

“When we launched the IATF in 2018, it was a bold experiment in connectivity. It was not only a commercial event, but rather a strategic tool to increase intra-African trade, which remains stubbornly low. As we prepare for the fifth edition of the IATF, we must ensure that it propels intra-African trade and helps Africa reposition itself in the global trade landscape. We should therefore aim very high in 2027, especially as the IATF takes place in Nigeria, the most populous African country and one of the continent’s largest economies. Let us make IATF 2027 a defining moment that ignites new momentum for Africa’s investment, industrialisation and trade,” she said.

Reflecting on the broader continental impact, Cynthia E. Gnassingbé-Essonam, Director of Private Sector Engagement and Communications at AfCFTA Secretariat, who represented H.E. Wamkele Mene, Secretary General, AfCFTA Secretariat, emphasised that Nigeria’s host of IATF2027 reinforces collective efforts to operationalise the AfCFTA and deepen regional value chains.

“Today’s ceremony marks an important milestone in our collective efforts to advance the objectives of the African Continental Free Trade Area. The Intra-African Trade Fair has established itself as Africa’s premier marketplace for trade and investment, bringing together businesses, investors and policymakers from across the continent and the diaspora. Nigeria’s host of IATF 2027 is both timely and significant, and we are confident it will deliver an impactful trade fair that reflects the ambition of the AfCFTA and the aspirations of African businesses,” she commended.

For more information about IATF2027 please visit www.IntrAfricanTradeFair.com

Distributed by APO Group on behalf of Afreximbank.

You may like

-

WPC-African Energy Week (AEW) Date Clash: Is Riyadh Playing Fair With Africa? (By Ajong Mbapndah L)

-

Radisson Hotel Group launches global long-stay proposition to accelerate growth in fast-growing extended-stay segment

-

Afreximbank extends EUR110-million facility to Chad in largest ever financing support to the country

-

Venezuela Energy Week Confirms 19 August Date for Houston Industry Showcase

-

Islamic Development Bank Institute (IsDBI) Secures New Patent for Smart Stabilization System from Intellectual Property Office of Singapore

-

Liberia to Preview Next Oil & Gas Licensing Round Strategy at Houston Investor Day

Energy

WPC-African Energy Week (AEW) Date Clash: Is Riyadh Playing Fair With Africa? (By Ajong Mbapndah L)

Published

3 hours agoon

August 11, 2026

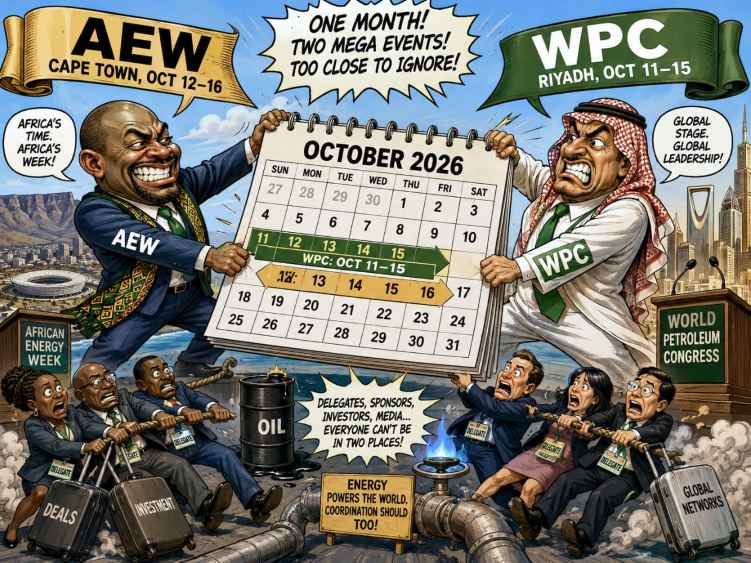

Africa’s Energy Voice Faces a Test in the WPC-AEW Showdown

African Energy Week has grown from an ambitious continental initiative into a powerful movement connecting governments, investors, national oil companies and global energy players around Africa’s development priorities. With its October 12–16, 2026 dates known well in advance, WPC Energy’s decision to reschedule its Riyadh Congress for October 11–15 raises uncomfortable questions about fairness, respect and whether Africa is still expected to accommodate decisions made elsewhere.

African energy leaders have every reason to ask a simple but uncomfortable question: why would one of the world’s biggest energy gatherings reschedule its 2026 congress into almost exactly the same window as African Energy Week when the Cape Town dates had long been known across the industry?

The 25th WPC Energy Congress will take place in Riyadh from October 11–15, 2026, while African Energy Week (AEW): Invest in African Energies runs in Cape Town from October 12–16. For four crucial days, the two gatherings will compete for many of the same ministers, national oil company executives, international oil companies, financiers, service companies, investors and media.

Calling that merely an unfortunate scheduling coincidence understates both the practical consequences and the message the decision inevitably sends to an African energy industry increasingly determined not to be treated as an afterthought.

AEW is not an obscure conference that unexpectedly appeared on an overcrowded international calendar. Its October 12–16 dates had already been communicated publicly in 2025 and continued to be promoted thereafter as the established dates for the next edition, giving governments, companies, sponsors and investors ample notice to organise their participation.

In energy circles, major conferences do not simply materialise a few weeks before opening day. Ministers block calendars, companies allocate sponsorship budgets, exhibitors reserve space, executives plan travel and governments prepare investment roadshows months in advance, which is why the suggestion that AEW’s dates could somehow have escaped attention is difficult to reconcile with how this industry operates.

This is especially true because of what African Energy Week has become. What the African Energy Chamber (AEC) has built in barely half a decade is not simply another annual conference but one of the strongest platforms yet created for Africans to articulate their own energy priorities, engage investors directly and challenge a global conversation that has too often spoken about Africa rather than with Africa.

AEW began in 2021 with roughly 1,700 delegates and rapidly expanded into a gathering attracting thousands of ministers, government officials, national oil companies, independent producers, international majors, financiers and service providers. The 2026 edition is positioning itself as another major step forward, reflecting the momentum the Chamber has built around investment, project development, dealmaking and African energy sovereignty.

Organisers are projecting more than 9,000 attendees, over 300 ministers and VIPs, more than 400 speakers and upwards of 1,500 companies for 2026. Those are not the numbers of a marginal regional conference but of an increasingly influential international energy marketplace built in Africa around African opportunities.

That growth matters because AEW has always carried a clear proposition: Africa’s energy choices must reflect Africa’s development realities. The continent cannot be expected to approach the transition from the same starting point as countries that industrialised using abundant fossil fuels and now enjoy universal or near-universal electricity access, sophisticated transport networks and mature economies.

African policymakers are wrestling with a different equation involving energy poverty, industrialisation, employment, population growth, food security and the enormous capital requirements needed to build modern economies. AEW has consistently provided them with a platform to say that oil and gas, alongside renewables, nuclear, hydropower, critical minerals and emerging technologies, must remain part of an African transition shaped by African needs.

The event has also moved far beyond speeches and ceremonial panels. Through investment forums, deal rooms, farmout discussions, NOC-IOC engagement, local-content programmes and financing conversations, AEW has increasingly sought to put licence holders and project developers face-to-face with investors capable of turning opportunities into producing assets and functioning infrastructure.

That emphasis is vital because Africa does not simply need another global conversation about energy. It needs exploration capital, pipelines, gas-processing facilities, refineries, power plants, transmission networks, renewable projects, industrial infrastructure and financing mechanisms capable of supporting them.

The African Petroleum Producers Organization’s growing role in the wider continental energy conversation, together with efforts surrounding African financing mechanisms, adds another strategic layer. African producers increasingly recognise that sovereignty over resources means little if every major project remains dependent on financing institutions outside the continent whose policies may not align with African development priorities.

AEW has become one of the places where that new confidence is expressed, and this is precisely why the Riyadh scheduling decision has landed so badly. Africa is no longer simply grateful to be invited into global energy conversations; it is building its own tables, filling its own rooms and increasingly attracting the same ministers, executives and investors sought by the traditional power centres of the industry.

WPC Energy is itself an important global institution and nobody needs to diminish its standing to recognise the problem. Precisely because it understands the importance of ministerial and CEO participation, WPC should also understand what happens when a congress is placed across the dates of another major gathering.

A petroleum minister cannot be in Cape Town and Riyadh simultaneously, an NOC chief cannot spend the same afternoon negotiating investment partnerships at AEW and participating in WPC sessions thousands of kilometres away, and companies with limited executive teams cannot pretend geography does not exist.

That raises an obvious question African stakeholders are entitled to ask: would the same decision have been taken so readily if the event affected were ADIPEC, CERAWeek or Gastech? Would a congress seeking many of the same ministers, CEOs and sponsors knowingly move directly over one of those dates and simply expect the organisers to absorb the consequences?

If such a collision would demand careful consultation elsewhere, Africa deserves to know why Cape Town appears different. Africa is not asking for the international calendar to be cleared every time it hosts an event, but there is an enormous difference between unavoidable congestion and moving a heavyweight gathering onto dates already occupied by a fast-growing continental platform.

The optics are made worse by the fact that cooperation, rather than confrontation, has existed before. In 2022, the African Energy Chamber and World Petroleum Council Canada signed a memorandum of understanding under which they agreed to support and promote each other’s conferences, including African Energy Week and the 2023 World Petroleum Congress, while cooperating on delegates, exhibitors, partners, webinars and industry dialogue.

That history makes the present collision more difficult to understand. Institutions connected to the WPC family understood enough about AEW’s importance to work with the AEC, promote each other’s platforms and encourage participation, so African stakeholders are justified in wondering how cooperation evolved into a calendar arrangement that now puts the two gatherings in direct competition.

WPC also has a significant history with Africa itself. Johannesburg hosted the 18th World Petroleum Congress in 2005, the first WPC Congress held on the continent, meaning Africa is hardly unfamiliar territory to the organisation and African petroleum institutions are certainly not strangers to the WPC ecosystem.

The African Energy Chamber itself has been reluctant to publicly turn the situation into a confrontation despite being approached about the issue. That restraint is noteworthy because an organisation that has rarely been shy about defending African energy interests could easily have escalated the dispute, yet its reluctance to comment should not be mistaken for an absence of concern across the wider industry.

The silence may actually make the questions louder. When an organisation built around forceful advocacy for African investment chooses caution, others will inevitably look more closely at what the scheduling decision means and why it happened.

Nigeria Faces an Uncomfortable Leadership Test

The scheduling collision becomes even more consequential when Nigeria enters the picture. As a continental economic heavyweight, one of Africa’s leading oil and gas producers and home to one of its deepest pools of indigenous energy companies, Nigeria’s voice carries enormous weight in determining how Africa positions itself in the rapidly changing global energy order.

Nigeria is not simply another producer attending conferences in Cape Town and Riyadh. It is the country chosen to host the Africa Energy Bank in Abuja, an institution conceived by the African Petroleum Producers Organization and Afreximbank to help close the financing gap facing African energy projects.

That gives Abuja a particular responsibility in debates about African energy sovereignty. The Africa Energy Bank represents precisely the kind of institutional independence that AEW has championed: African capital mobilised to support African projects at a time when traditional international financiers have become increasingly reluctant to fund oil and gas development on the continent.

Nigeria is also home to perhaps the most dramatic symbol of Africa’s changing energy ambitions in Aliko Dangote and his refinery complex. The significance of what Dangote is building goes well beyond one businessman, one company or one refinery, particularly as his industrial interests continue expanding their footprint across Africa.

The Dangote Refinery challenges a decades-old African model in which crude is exported, value is created elsewhere and expensive refined products are imported back into the continent. It represents a different proposition: African resources processed on African soil, creating African industrial capacity and allowing a greater share of the value chain to remain on the continent.

Nigeria consequently sits at the intersection of almost every major argument AEW has been making about Africa’s energy future: indigenous ownership, local processing, energy security, African financing, domestic gas development, investment reform and the transformation of natural resources into industrial capacity rather than merely export revenues.

Its relationship with African Energy Week has also been deep and highly visible. Successive Nigerian government officials, regulators and corporate leaders have used AEW to promote investment opportunities, explain reforms and engage international capital, while Nigerian companies have maintained substantial presences through choice exhibition spaces, speaking engagements, panels, sponsorships and dealmaking.

That engagement has continued under President Bola Tinubu’s administration. Presidential Special Adviser on Energy Olu Verheijen has become a prominent voice around the gathering, while Minister of State for Petroleum Resources Heineken Lokpobiri and other senior Nigerian officials have used AEW to promote the country’s investment reforms and energy opportunities.

The Nigerian corporate contingent announced for 2026 is equally formidable. Oando Group Chief Executive Adewale Tinubu is among the high-profile industry leaders expected, alongside executives from some of Nigeria’s most important indigenous operators and international companies active in the country’s upstream sector.

Renaissance Africa Energy Company is participating as a Gold Sponsor and is expected to showcase a growth strategy involving a $15 billion investment drive following its acquisition of major former Shell onshore assets. Its presence embodies exactly the kind of African corporate transformation that AEW was created to showcase.

Dr. Nosa Omorodion, SLB’s Country Director for Nigeria, is also due to receive AEW’s Lifetime Achievement Award recognising more than three decades of contributions to technology, local content, production optimisation and human-capital development. Taken together, the Nigerian presence makes Cape Town one of the most significant international showcases of Nigeria’s changing energy industry outside Nigeria itself.

That is why Nigeria now finds itself in an unusually uncomfortable position. On October 11, one day before AEW begins, Nigeria will join Saudi Arabia and Italy as a co-host of the 17th International Energy Forum Ministerial Meeting in Riyadh, a gathering bringing together energy ministers, industry leaders and international organisations to discuss energy security, market stability, investment and the future of global energy.

There is nothing inherently contradictory about Nigeria participating in both. Indeed, a country of Nigeria’s importance should be represented at every serious table where the future of global energy is being discussed, and its role as an IEF17 co-host is itself recognition of Abuja’s international standing.

The problem is what happens immediately afterwards. WPC begins its principal programme in Riyadh on October 12, the same day AEW opens in Cape Town, potentially turning Nigeria’s legitimate global leadership role into a difficult balancing act between an international gathering it is helping co-host and an African platform it has spent years helping build.

That puts Abuja in a position it did not create alone, but one from which legitimate leadership questions arise. Did Nigerian authorities, particularly at ministerial and senior government level, raise concerns about the scheduling conflict when Riyadh’s plans were being assembled?

Given Nigeria’s role as an IEF17 co-host and its considerable diplomatic weight in global petroleum affairs, did Abuja caution its partners about the consequences of placing the wider Riyadh programme directly against African Energy Week? Did policymakers weigh the African optics of appearing to prioritise a foreign gathering over a platform that Nigerian officials and companies have helped establish as one of the unmistakable symbols of Africa’s energy renaissance?

Could Nigeria have used its influence behind the scenes to encourage coordination before the clash became unavoidable? These are questions, not accusations, and there is no public evidence establishing what conversations may have occurred privately between Abuja, Riyadh, the IEF, WPC Energy or AEW organisers.

Nigeria should therefore not be condemned for diplomacy whose details are not publicly known, but leadership is judged partly by the signals it sends, particularly when competing interests collide. Nigeria’s position means it cannot comfortably treat this as somebody else’s scheduling dispute.

At moments like this, the continental giant cannot afford to send mixed signals about where it stands on Africa’s energy fortunes and future. This does not mean Nigeria should boycott Riyadh, retreat from international engagement or choose Cape Town against the rest of the world; such an approach would be unrealistic and counterproductive.

The stronger expression of Nigerian leadership would be to demonstrate that global engagement and African solidarity are complementary rather than competing obligations. Abuja can play an important role in Riyadh while making unmistakably clear through senior representation, corporate participation and diplomatic engagement that AEW remains a strategic African platform worthy of support.

That distinction matters because other African governments will be watching. If Nigeria, host of the Africa Energy Bank and home to some of the continent’s most ambitious indigenous energy companies, appears indifferent when an African platform is placed under avoidable competitive pressure, smaller producers may reasonably wonder who will defend African institutions when their interests collide with larger global powers.

Nigeria’s strength creates expectations. It has the market, population, diplomatic reach, petroleum industry, corporate champions and increasingly the refining capacity to provide leadership far beyond its borders, and that leadership becomes most valuable precisely when Africa’s interests require a clear voice.

Geopolitics Makes the Timing Even More Significant

Africa does not want to remain the continent whose resources are strategically important but whose priorities are negotiable

The dispute cannot be separated from geopolitics. Energy security has again become inseparable from national security, with instability around major producing regions and strategic shipping routes reminding governments how quickly global supply assumptions can change.

The Red Sea, Strait of Hormuz and wider Middle East remain central to global energy flows, while competition among the United States, China, Europe, Russia, Gulf powers and emerging economies increasingly encompasses oil and gas, LNG, critical minerals, technology, infrastructure and control of strategic supply chains.

That geopolitical environment should make African energy more strategically important, not less. West Africa’s Atlantic Basin resources, new discoveries in Namibia, established producers such as Nigeria and Angola, major gas developments from Senegal and Mauritania to Mozambique, and expanding refining capacity strengthen the argument that diversified African supply can contribute meaningfully to global energy security.

Africa should therefore not be treated as a secondary room in the global energy house just when geopolitics is demonstrating the value of diversification. When traditional supply corridors are threatened, the world suddenly remembers the strategic importance of African barrels and African gas, yet African producers have every right to ask whether that importance is reflected in the way their institutions and platforms are treated when crises subside.

This is where the sense of disrespect becomes larger than a conference calendar. Africans have spent decades watching outside actors arrive when resources are required, disappear when development financing is needed, return with prescriptions about what the continent should stop producing and then rediscover African hydrocarbons whenever geopolitical shocks make alternative supplies attractive.

Africa does not want to remain the continent whose resources are strategically important but whose priorities are negotiable, whose minerals are indispensable but whose industrialisation can wait, and whose conferences matter only until a larger institution decides it wants the same week.

The frustrations are not invented. Angola’s withdrawal from OPEC in 2023 after disagreements over production quotas became one of the clearest recent examples of an African producer deciding that participation in an established international institution was no longer worthwhile if its national interests could not be adequately accommodated.

Whether one agreed with Luanda’s decision or not, the lesson was unmistakable: African governments are increasingly willing to defend national interests when established structures no longer appear responsive to them. That same confidence is visible in calls for greater local refining, stronger African financial institutions, more assertive national oil companies and greater domestic value addition.

The Dangote Refinery is perhaps the most visible symbol of this change. For generations, one of Africa’s largest crude producers exported its oil while importing huge volumes of refined products, but the rise of massive domestic refining capacity represents a broader continental ambition to stop exporting resources in their least valuable form and importing the value-added products back at a premium.

AEW sits squarely within this changing African mindset. It argues that the continent should produce more where sensible, process more at home, finance more of its own projects, negotiate harder with international partners and ensure that energy development produces electricity, jobs, infrastructure and industrial capacity for Africans.

That is why the event has become something larger than its organiser. The African Energy Chamber may provide the machinery, but the movement around AEW increasingly reflects frustrations and ambitions shared across governments, NOCs, indigenous companies and a generation of African energy professionals tired of being told that their continent must remain permanently accommodating.

From Cape Town to Caracas: The Chamber’s Reach Is Expanding

The Chamber’s response to the scheduling controversy has not been to retreat into a defensive continental posture. Its recent activities demonstrate almost the opposite: an increasingly ambitious effort to connect African energy interests with governments, investors and markets far beyond the continent.

That international outreach has been particularly visible in Venezuela. The AEC has developed a structured relationship with Caracas involving investment promotion, technical cooperation, capacity building and engagement across the hydrocarbon value chain, including high-level dialogue with Venezuela’s Acting President Delcy Rodríguez, petroleum authorities and executives of state-owned PDVSA.

The relationship progressed from high-level engagements earlier in 2026 into another AEC working mission to Caracas from August 3–5. The Chamber’s return to Venezuela, coupled with its involvement in international efforts promoting Venezuela’s energy investment opportunities, illustrates an organisation increasingly capable of carrying African energy diplomacy beyond traditional Western and Gulf centres.

The symbolism is difficult to miss. An organisation established to advance African energy interests is now engaging at senior political and industry levels in the country possessing the world’s largest proven oil reserves, building bridges between African producers and one of Latin America’s most consequential petroleum states.

That growing relationship also reflects a wider South-South strategy. Cooperation between the AEC and Venezuelan institutions has involved links with APPO and discussions around investment, technology transfer, workforce development, gas commercialisation and opportunities for African operators, extending the Chamber’s reach from African advocacy into international energy diplomacy.

The Chamber has simultaneously been strengthening relationships elsewhere. Its engagement with Mozambique’s national oil company ENH, for example, has focused on investment, local content and private-sector participation as Mozambique advances a gas industry anchored by more than $50 billion in major LNG developments.

These engagements reveal something important about the movement behind AEW. The Chamber is not arguing that Africa should isolate itself from global energy markets or replace dependence on one bloc with dependence on another; it is seeking to broaden Africa’s partnerships and give African companies, governments and institutions more options.

That is precisely what energy sovereignty should mean in an increasingly multipolar world. Africa should be able to engage Riyadh, Caracas, Houston, London, Beijing, Moscow, Abu Dhabi and every other serious energy centre while maintaining strong institutions of its own.

The Chamber’s growing international appeal consequently makes the WPC scheduling clash even more puzzling. AEW is not a retreat from global engagement; it is Africa’s contribution to it.

AEW Pushes Ahead With Growing Confidence

If the scheduling controversy was expected to unsettle African Energy Week, there is little outward evidence that it has done so. Preparations in Cape Town are proceeding at full speed, with the Chamber continuing to announce ministers, government officials, global executives, indigenous operators, sponsors and investors for October.

Nigeria’s announced participation alone underlines that confidence, while representation from across the continent and beyond continues to expand. AEW’s strategy appears to be less about engaging in a public war of words with WPC and more about demonstrating through participation, investment announcements and partnerships that the platform has developed enough institutional weight to withstand competition.

The Chamber’s reluctance to publicly escalate the scheduling dispute is notable in this context. An organisation known for forceful advocacy on African energy matters has chosen not to turn the issue into an open institutional confrontation, but its restraint should not be interpreted as weakness or evidence that the clash is inconsequential.

Its activities suggest an organisation looking well beyond Cape Town. The AEC has been pursuing engagements across Africa and internationally, from Mozambique and other emerging African energy markets to Venezuela and global investment centres, reflecting an increasingly broad strategy for connecting African energy interests with capital, technology and partnerships wherever opportunities emerge.

That strategy becomes increasingly relevant as geopolitics reshapes energy flows. Africa enters this environment with resources everyone wants: major oil and gas reserves, extraordinary renewable potential, critical minerals required for the technologies driving the energy transition and one of the world’s largest future sources of energy demand.

The continent therefore has leverage, but resources alone do not automatically translate into power. Power comes when countries coordinate, institutions mature, capital is mobilised, resources are processed locally and African governments negotiate from a clearer understanding of their collective strategic value.

That is the deeper significance of African Energy Week and why the WPC scheduling conflict matters. AEW represents part of Africa’s effort to build the institutional infrastructure required to convert resources into influence.

Nigeria is central to whether that effort succeeds. Abuja’s hosting of the Africa Energy Bank, the rise of indigenous companies such as Oando, Renaissance Africa Energy and Heirs Energies, the scale of the Dangote industrial project and the government’s efforts to attract new upstream investment make the country an indispensable pillar of Africa’s emerging energy architecture.

The scheduling collision consequently presents Nigeria with something larger than a diary problem. It is a test of how Africa’s most consequential energy powers navigate a world in which they want strong relationships with Riyadh, Washington, London, Abu Dhabi, Beijing, Caracas and other global centres while simultaneously strengthening institutions created to advance African priorities.

There should be no contradiction between the two, provided international partnerships respect Africa’s institutions rather than weaken them. That principle returns the debate to WPC and the question of whether the same scheduling approach would have been considered acceptable if the affected gathering were ADIPEC, CERAWeek, Gastech or another event whose importance to the international energy calendar nobody questions.

If the answer is doubtful, Africans are justified in asking why AEW was apparently expected to absorb the collision. Africa has reached a stage where being strategically valuable while institutionally disregarded is no longer acceptable.

Its resources cannot be indispensable during geopolitical crises while its platforms become expendable when calendars are drawn up, and its governments cannot be courted for barrels, gas and minerals while the institutions they are building receive a lesser standard of consideration.

Riyadh has every right to host a major global energy gathering. Saudi Arabia has enormous influence in petroleum markets, world-class infrastructure and legitimate ambitions to convene policymakers and industry leaders around questions that will shape the future of energy.

Cape Town has exactly the same right to host Africa’s flagship gathering without having its dates treated as expendable. An equitable global energy system cannot mean that established centres automatically receive priority while emerging African platforms are expected to absorb disruption.

WPC’s own 2026 theme, “Pathways to an Energy Future for All,” emphasises inclusion and shared participation, yet inclusion cannot remain an attractive slogan printed across conference materials while practical decisions place one of Africa’s most important energy gatherings at a competitive disadvantage.

An energy future “for all” must include respect for the platforms Africans have built for themselves. It cannot require African ministers to choose between pitching investment opportunities in Cape Town and attending discussions in Riyadh, nor should African companies have to decide whether scarce marketing and travel budgets should follow continental priorities or global prestige.

AEW has earned its place on the international calendar. The Chamber has built momentum around it, African governments have given it political credibility, companies have brought investment propositions to it and international partners have recognised its growing significance.

That is precisely why the WPC scheduling decision deserves scrutiny rather than polite silence. If AEW were still small and irrelevant, nobody would care when another conference took place, but the problem exists precisely because Cape Town now competes for ministers, CEOs, investment capital, project announcements and international attention.

Perhaps that is the clearest indication of how far AEW has come. Africa has created a platform important enough for a scheduling collision to have global consequences, and the appropriate response from established institutions should be engagement and coordination rather than an expectation that Africa will simply adjust.

Could this have been done to ADIPEC without controversy? Could CERAWeek suddenly find another global heavyweight targeting virtually the same ministers and CEOs without questions being asked, or could Gastech reasonably be expected to shrug when a comparable institution moves directly across its programme?

Those questions expose the underlying issue. Africa does not seek privileges that others do not enjoy; it simply refuses to be held to a lower standard of consideration.

For too long, the continent has been told to be patient, flexible and grateful while decisions affecting its resources, financing and development have been made elsewhere. The rise of AEW, African-led financing initiatives, stronger NOCs and increasingly assertive governments suggests that era is ending.

The WPC-AEW dispute is therefore not really about Cape Town versus Riyadh. It is about whether a changing global energy order is prepared to recognise African agency once Africa becomes strong enough to insist upon it.

WPC may regard October 11–15 simply as its new dates, but African stakeholders are entitled to see the move through the prism of a much longer history. The dates of AEW were known, cooperation had existed in the past, the consequences of the overlap are obvious, and the international energy industry understands better than almost any other sector that calendars involving ministers and CEOs are strategic assets rather than administrative details.

Africa is not asking for special treatment, nor is it asking Riyadh to abandon its ambitions. It is asking for the basic professional courtesy and institutional respect that any serious global platform would expect for itself.

At a time when geopolitical turmoil is reminding the world of Africa’s strategic energy value, disregarding one of the continent’s most important energy platforms is particularly ill-judged. Africa’s oil, gas, minerals, renewable resources and growing markets cannot be indispensable when the world needs them but peripheral when Africans demand a meaningful voice over how those resources are developed.

African energy leaders will continue travelling to Riyadh, Houston, Abu Dhabi, Caracas, London and other global centres because partnership remains essential. But they will increasingly do so as representatives of a continent building its own institutions and expecting those institutions to be respected.

AEW has become one of those institutions, and the African Energy Chamber has built a movement around the conviction that Africa must stop apologising for pursuing investment, industrialisation and energy security. Its growing reach from Cape Town to Abuja, Maputo, London and Caracas shows that the movement is no longer confined to Africa but is increasingly participating in the wider diplomacy and dealmaking of global energy.

The WPC scheduling controversy now provides an unexpected test of whether the wider global energy establishment has absorbed the other half of that message: Africa should no longer be taken for granted.

The real question heading into October is therefore larger than which event draws the bigger crowd. It is whether institutions that speak so readily about partnership, inclusion and a global energy future are prepared to demonstrate those principles when Africa’s own priorities require accommodation rather than rhetoric.

Distributed by APO Group on behalf of Pan African Visions.

Business

Radisson Hotel Group launches global long-stay proposition to accelerate growth in fast-growing extended-stay segment

Published

3 hours agoon

August 11, 2026

The new proposition positions Radisson Hotel Group at the forefront of one of the hospitality industry’s fastest-growing segments, offering a dedicated B2B solution for long-stay bookings through corporate and partner channels, with a focus on simplified booking, structured pricing, and consistent guest experience

Bringing together participating hotels with apartment units across the Group’s portfolio, the initiative introduces a more unified and seamless approach to long stays – ensuring consistency in service, comfort, and flexibility for guests, while supporting corporate partners with simplified access to extended-stay solutions. The offering introduces a structured yet flexible framework that makes long stay bookings easier to buy, manage, and experience.

Designed primarily for B2B partners – including relocation companies, travel management companies, and corporate travel buyers – the proposition enables access to dedicated long stay rates, standardized booking conditions, and aligned commission structures across participating hotels, removing the need to negotiate individual agreements.

At the same time, guests benefit from a tailored extended stay journey, including dedicated hotel contacts, personalized pre-arrival planning, and amenities designed specifically for longer stays. Importantly, the approach supports a seamless guest journey through both negotiated corporate agreements and long stay bookings, ensuring that travelers receive a consistent experience regardless of how their stay is sourced. By aligning commercial and operational elements, Radisson Hotel Group strengthens its ability to deliver on guest expectations across brands and markets.

The launch responds to changing travel patterns, with companies increasingly requiring flexible accommodation for international assignments, infrastructure projects, consulting engagements, healthcare placements and workforce mobility. As demand shifts beyond traditional transient travel, the Group is investing in solutions that enhance the guest journey, while helping partners secure higher-value bookings with greater efficiency.

Long Stays by Radisson Hotels gives our partners a simpler and more competitive way to access this growing market

“Long Stays by Radisson Hotels gives our partners a simpler and more competitive way to access this growing market,” said Gianni Di Fede, Chief Commercial Officer at Radisson Hotel Group. “By combining structured commercial terms with a consistent guest experience, we’re making it easier to win and service long-stay business at scale, while strengthening customer loyalty.”

Structured commercial model for long-stay business

At the core of the proposition is a dedicated commercial model featuring tiered pricing based on length of stay, with defined conditions and partner-friendly commission structures. This supports faster response times and greater transparency for booking agents and corporate clients. The offer reinforces its value through Radisson Rewards, where eligible bookers and planners benefit from an additional 20% points incentive on long stay bookings, strengthening loyalty and engagement within the segment.

The offer integrates with existing distribution channels, including GDS and corporate agreements, allowing partners to book through established procurement and travel management processes without additional complexity.

Delivering a consistent extended-stay experience

In addition to commercial enhancements, Long Stays by Radisson Hotels focuses on elevating the guest experience for longer stays. Participating hotels provide personalized pre-arrival planning, dedicated contacts, flexible housekeeping services, and in-room solutions designed for extended use.

These elements create a consistent, home-like environment that supports feeling at ease, productivity, and flexibility throughout the guest journey.

Supporting growth in key markets

The initiative is supported by strong extended-stay demand in major global markets across EMEA and APAC, including Dubai, Riyadh, Zurich, and Amsterdam. By increasing length of stay and improving conversion for long-term bookings, the proposition supports revenue optimization and stronger partner relationships.

The program is now available for participating hotels across the Radisson Hotel Group portfolio. Visit our website here (https://apo-opa.co/3S3IFu1) for more information.

Distributed by APO Group on behalf of Radisson Hotel Group.

Business

Afreximbank extends EUR110-million facility to Chad in largest ever financing support to the country

Published

3 hours agoon

August 11, 2026

The facility will promote trade flows, enhance economic resilience, and support the implementation of strategic trade-enabling infrastructure projects that are critical to advancing Chad’s long-term trade, economic transformation, and development objectives

The facility agreement, signed on August 5,2026 at the Afreximbank Headquarters in Cairo, Egypt by Dr. George Elombi, President and Chairman of the Board of Directors of the Bank, and Honourable Tahir Hamid Nguilin, Senior Minister, Minister of Finance, Budget, Economy, Planning and International Cooperation of Chad, provides for the proceeds of the facility to be utilised by the government to support trade-enabling infrastructure projects, as approved under the Country’s 2026 Finance Law.

The facility will promote trade flows, enhance economic resilience, and support the implementation of strategic trade-enabling infrastructure projects that are critical to advancing Chad’s long-term trade, economic transformation, and development objectives.

The deal further strengthens the strategic partnership between Afreximbank and the Government of Chad by supporting initiatives that promote local value addition, industrialisation and economic transformation in the country and the region.

The signing of this EUR 110 million financing agreement with Afreximbank marks a major milestone in strengthening the partnership between Chad and the Bank

This intervention is aligned with the Memorandum of Understanding (MoU) signed between the Government of Chad and Afreximbank in June 2025, which established a strategic framework for collaboration across key sectors, including the development of Chad’s agropastoral potential, export-oriented agriculture, gold trading, the navigability of Lake Chad, refined petroleum trading, and refinery development.

Afreximbank’s President and Chairman of the Board of Directors, Dr George Elombi, described the facility as an important milestone in the Bank’s partnership with the Government of Chad:

” Afreximbank is pleased to be a critical actor in Chad’s economic transformation journey and commends the government for the bold agenda to structurally transform the national economy. The credit facility is part of a financing programme aimed at supporting the government to deliver on priority projects, including special industrial zones for textile manufacturing and meat processing, transport infrastructure to connect Chad to Egypt and Libya as well as power generation, creation of crude refining capacity, and creation of transport and maritime economic opportunities in Lake Chad, among others. These investments will contribute to changing the structure of the Chadian economy and create sustainable employment and wealth for the Chadian people. With these investments, we are steadily placing Africa’s development future in the hands of the African people.”

Honourable Tahir Hamid Nguilin, Senior Minister, Minister of Finance, Budget, Economy, Planning and International Cooperation of Chad added: “The signing of this EUR 110 million financing agreement with Afreximbank marks a major milestone in strengthening the partnership between Chad and the Bank. This financing demonstrates Afreximbank’s renewed confidence in our country’s economic prospects and its ability to harness its potential. The resources mobilized will contribute to financing critical trade-enabling projects included in our national budget, particularly in the areas of infrastructure and the development of trade.

“We are particularly committed to transforming our natural wealth and economic potential into tangible trade opportunities for our economy and our people. This transaction also reflects our determination to diversify our financial partnerships and strengthen regional and continental economic integration. The Government of Chad looks forward to continuing this dynamic partnership with Afreximbank in support of sustainable, inclusive and job-creating growth.”

Chad’s economic transformation is steadily reshaping its economic future through a combination of strategic reforms, agricultural expansion, and sustained investment in its oil sector. Once heavily reliant on crude oil revenues, the country is now making progress towards building a more diversified and resilient economy. This transformation has earned international recognition, with the World Bank upgrading Chad’s 2026 economic growth forecast to 5.2 per cent.

Distributed by APO Group on behalf of Afreximbank.

Trending

-

Business4 days ago

Business4 days agoEnergy Capital & Power Establishes London Entity, Expanding Global Platform for Energy and Mining Events

-

Business4 days ago

Liberia to Preview Next Oil & Gas Licensing Round Strategy at Houston Investor Day

-

Business4 days ago

Business4 days agoBeyond Stabroek: Guyana’s Offshore Basin Attracts New Wave of Exploration Investment

-

Business4 days ago

Guyana’s Next Wave of Offshore Projects Sets the Stage for Caribbean Energy Week Launch

-

Business21 hours ago

Islamic Development Bank Institute (IsDBI) Secures New Patent for Smart Stabilization System from Intellectual Property Office of Singapore

-

Energy21 hours ago

Venezuela Energy Week Confirms 19 August Date for Houston Industry Showcase

-

Business3 hours ago

Radisson Hotel Group launches global long-stay proposition to accelerate growth in fast-growing extended-stay segment

-

Business3 hours ago

Afreximbank extends EUR110-million facility to Chad in largest ever financing support to the country